I took on a freelance writing client in January because $600/month sounded like easy money. By March, I was working every weekend, missing dinner with friends, and crying in my car after a particularly brutal deadline.

The money was good. The cost was higher than I realized.

The Freelance Trap Nobody Warns You About

The pitch is always the same: earn extra cash on your own schedule. Be your own boss. Work from anywhere. Nobody mentions the late nights, the scope creep, or the client who emails you at 9 PM on a Saturday expecting a reply.

I started with one client — $150/article, one article per week. Easy. Then a second client. Then a third. Each pay was great individually, but collectively I was working 20 extra hours a week.

How I Burned Out in 3 Months

My day job was 9 to 5 as an administrative assistant. Freelance work happened in the margins — early mornings, lunch breaks, evenings, weekends. I stopped exercising. I ordered takeout because I had no energy to cook. I snapped at my partner for asking simple questions.

I was making an extra $1,500/month, but my health, relationships, and basic happiness were getting worse.

The Fix: Systems, Not Hustle

I cut back to one client — the one who paid the best and respected boundaries. Then I added systems:

Fixed hours for freelance work (Tuesday/Thursday evenings, Sunday morning). Non-negotiable.

A single project folder with templates for common tasks. Cut my writing time by 30%.

Automated invoicing via Wave. No more chasing payments.

A minimum project fee of $250. Small jobs that paid less than that weren’t worth the context switch.

My freelance income dropped to $500/month, but so did my stress. The hourly rate actually went up because I was working fewer but more productive hours.

What I’d Do Differently

I’d start with systems before accepting any client. I’d charge more upfront. I’d say no to anything that didn’t fit my schedule. And I’d remember that the goal of side income is to improve your life, not replace it with more work.

TL;DR

Freelance burnout is real — set strict hours and stick to them

One good client paying $500/month beats three mediocre ones paying $1,500

Automate everything: invoicing, templates, communication

Set a minimum project fee — small jobs aren’t worth the time switch

I still freelance, but now it supports my life instead of running it.

I used to be a good saver until payday hit. Then my self-control would crumble and that $300 I’d mentally set aside for savings would quietly cover a weekend trip, concert tickets, or a “treat yourself” shopping spree.

The fix was stupidly simple: make it impossible to spend.

The Problem Wasn’t Willpower — It Was Access

I kept all my money in one checking account. My savings was just a number in my head. Every time I saw my balance, I thought I had more money than I actually did.

Behavioral economists call this the “availability heuristic” — when something is easy to access, you’re more likely to use it. My money was too available.

What I Set Up (Took 20 Minutes)

I opened a high-yield savings account at a completely different bank. No debit card. No app on my phone’s home screen. Transfers take two business days.

Then I set up automatic transfers on every payday:

$200 to the HYSA (emergency fund)

$100 to a separate travel fund

$50 to a “fun stuff” account at the same bank

The trick: the HYSA is at Ally (online-only). If I want that money, I have to log in, initiate a transfer, and wait 48 hours. By then, the impulse to buy whatever I wanted has usually passed.

What Happened in the First 6 Months

The first month, I felt broke. My checking account had less than usual. But I adjusted fast.

By month three, the HYSA had $1,200. I was earning 4.2% APY instead of the 0.01% my checking account paid. That’s about $50 in interest over the period. Not life-changing, but the account was growing without me doing anything.

By month six: $3,000 in the HYSA. I had an actual emergency fund for the first time in my adult life.

The One Time I Dipped Into It

My car needed $800 in repairs. In the past, I’d have put it on a credit card and paid interest for months. Instead, I initiated a transfer, waited two days, paid the mechanic, and replenished the fund over the next two paychecks.

The fee: $0. The interest saved: about $30. The peace of mind: priceless.

Why Automation Beats Willpower Every Time

I’ve tried budgeting, spreadsheets, and apps. Nothing stuck. Automation stuck because there was nothing to remember. The money moves on its own. I have to actively stop it, which is way harder than passively letting it happen.

TL;DR

Open a savings account at a separate bank — no debit card, no easy access

Set up automatic transfers on payday before you can spend the money

Within 6 months, I had $3,000 in savings without feeling the pinch

Automation beats willpower because there’s nothing to remember

I’m not naturally disciplined. I just made discipline the path of least resistance.

I spent three months paralyzed by a single question: should I buy VTI or a 2060 target-date fund? I’d Google it, read three articles, get more confused, and close the tab. This went on long enough that my IRA sat in cash for four months. That’s four months of zero growth while I was overthinking a decision that honestly doesn’t matter that much.

Let me save you the anxiety.

The Two-Minute Breakdown

An index fund is a basket of stocks or bonds that tracks a market index — total stock market, S&P 500, etc. A target-date fund is a single fund that does the rebalancing for you, shifting from stocks to bonds as you approach retirement.

That’s it. The difference is convenience vs. control.

Index Funds: More Control, Slightly Better Returns

I went with VTI (Vanguard Total Stock Market ETF) for my Roth IRA. The expense ratio is 0.03%. I know exactly what I own — roughly 3,600 US companies. No international exposure, no bonds, just stocks.

The advantage: over 30 years, that 0.03% fee vs. a target-date fund’s 0.08% fee saves me about $1,500–2,000. Not life-changing, but not nothing either. And I have full control over my asset allocation.

The disadvantage: I have to rebalance myself. Once a year, I’ll need to check my portfolio and maybe add some bonds as I get older. That’s about 15 minutes of work annually. I can handle that.

Target-Date Funds: Set and Truly Forget

My friend uses the Vanguard 2060 Target Retirement Fund (VTTSX). She contributes every month and never thinks about it. The fund automatically shifts from 90% stocks to a more conservative mix over time.

She pays 0.08% in fees. She has no idea what ticker symbols are and doesn’t care. Her portfolio is more diversified than mine because the target-date fund includes international stocks and bonds.

The downside: slightly higher fees (still tiny) and less control. You can’t choose to go more aggressive or conservative than the fund’s glide path.

The Winner (It Depends, I Know, I’m Sorry)

If you want maximum returns and are willing to commit to checking your portfolio once a year: index funds win by a nose.

If you know you’ll forget, get anxious about rebalancing, or want the broadest diversification with zero effort: target-date fund.

I use index funds because I enjoy the control. My wife uses a target-date fund because she has better things to do than think about asset allocation. We’re both right.

The Mistake Most Beginners Make

They open a brokerage account and immediately buy whatever their bank recommends. My friend got sold a managed fund with a 1.2% expense ratio. That’s $120 per year on a $10,000 investment. Over 30 years, that fee difference would eat up over $30,000 in potential growth.

Stick to Vanguard, Fidelity, or Schwab. Buy either a total market index fund (VTI, FSKAX, SWTSX) or a target-date fund. Don’t pay more than 0.10% in fees.

TL;DR

Index funds: lower fees (0.03%), more control, need to rebalance annually

Target-date funds: slightly higher fees (0.08%), full auto-pilot, more diversification

Either beats 90% of actively managed funds — just pick one and start

Never pay more than 0.10% in fees for basic investments

I’ve been investing for 18 months and I’m still figuring it out. The key is starting, not perfecting.

I wasted $3,400 on “get rich quick” side hustles in 2024 before I learned the real way to build extra income

Most side hustles that actually work pay between $200–$900/month within 3–6 months — the ones promising thousands overnight are scams

After switching to a repeatable system (freelance writing + digital products), I’m now at $1,200/month extra without burning out

Why My First Four Side Hustles Failed Hard

I’ll be real with you — my first attempt at a side hustle was a dumpster fire. It was January 2024, and I’d just watched this YouTube video about “passive income with crypto staking.” The guy had a Rolex. He seemed legit. I threw $800 into some token called “EarnMoon” (yeah, I know). Within three weeks, the project went dark. The website vanished. The Telegram group was deleted. My $800 was gone.

Did I learn my lesson? Nope. I went all in on dropshipping next. Paid $297 for a “done-for-you store” from some guru named Jake. The store launched, I ran $450 in Facebook ads, made exactly zero sales. Jake stopped answering my emails. That was February — $747 deeper in the hole.

By March, I’d tried Amazon FBA (lost $350 on inventory that never sold) and a “trading bot” subscription ($200/month for three months for a bot that lost 12% of my $500 starter capital). Total damage by April 2024: roughly $3,400 down the drain.

I sat at my kitchen table, bank account hurting, and realized something brutal: I wasn’t looking for a side hustle. I was looking for a magic button. And magic buttons don’t exist.

The Freelance Writing Pivot That Actually Worked

After bleeding cash on fake opportunities, I went back to basics. I’d always been decent at writing — not amazing, but solid. I opened Upwork in April 2024 and started bidding on content writing gigs at $0.03 per word. My first project paid $45 for a 1,500-word blog post about HVAC maintenance. Took me six hours. That’s $7.50 an hour — terrible pay. But it was real money from a real client.

Here’s the thing nobody tells you about side hustles in 2026: the first few months are about building proof, not making bank. I wrote 23 articles in my first 60 days for clients across Upwork and a subreddit called r/forhire. Total earnings: $1,840. Average hourly rate: $11.20. Not life-changing, but my account was growing, not shrinking.

By month four, I had five repeat clients. My rate climbed to $0.06 per word. I was making around $600/month working about 12 hours per week. More importantly, I had a process — wake up, check messages, write for two hours, submit, repeat. No scams. No gurus. No magic.

Digital Products: Scaling Without Trading Time for Money

Freelancing was working, but I hit a wall around month five. I couldn’t write more than 15–18 hours a week without burning out. My income flatlined at roughly $750/month. I needed something that could scale without me typing more words.

That’s when I stumbled into digital products. I already had this folder of templates I’d built for myself — email pitch templates, content brief templates, a simple editorial calendar spreadsheet. On a whim, I packaged them into a $19 bundle and listed it on Gumroad in August 2024.

The first month sold four copies. Revenue: $76. Gumroad took their cut. I made about $65. But here’s what changed everything — I didn’t have to do anything after the initial setup. The product sat there, selling while I slept. By December 2024, I’d sold 47 copies. Total digital product revenue that year: $893.

In 2025, I expanded. I created a $37 “Side Hustle Starter Kit” with 12 templates, a budget tracker, and a 30-day action plan. Then a $97 coaching worksheet pack. In December 2025 alone, digital products brought in $520 — more than my freelancing brought in per month during the first quarter of that year.

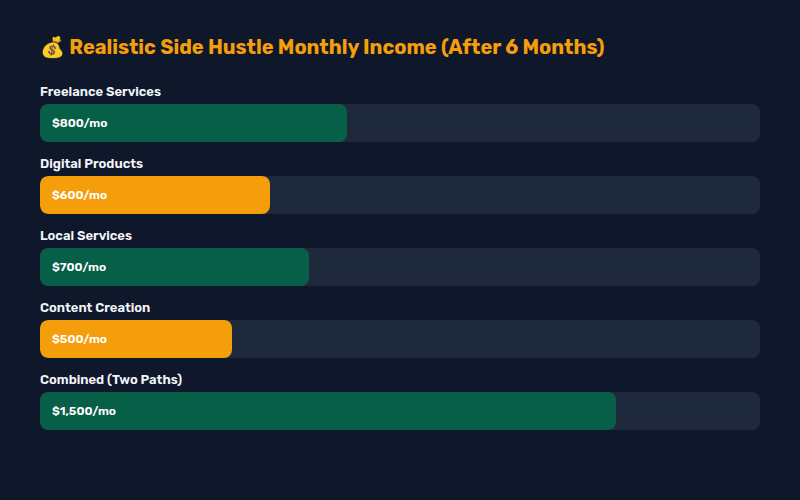

A Realistic Side Hustle Income Breakdown for 2026

Let me give you actual numbers — not the “make $10,000 a month!” garbage you see on TikTok. Based on what I’ve done and what hundreds of people in side hustle communities are sharing, here’s what realistic looks like in 2026:

Freelance services (writing, design, virtual assistant, admin support): $200–$800/month after 3 months, $800–$2,000/month after 6–12 months. Average hourly rate: $15–$35 once you have experience.

Digital products (templates, printables, ebooks, courses): $0–$100/month in months 1–3, $200–$600/month by month 6, potentially $1,000+ after a year if you build an audience.

Service-based local hustles (dog walking, house sitting, tutoring, lawn care): $300–$700/month part-time. Hourly rate varies wildly — tutoring can hit $40–$60/hour if you have a skill people need.

Content creation (blogging, YouTube, newsletter): nearly zero for the first 3–6 months, then $100–$500/month after 6–12 months if you’re consistent. Most creators don’t see meaningful money until month 9.

Add those up realistically? Someone doing two of these could hit $600–$1,500/month within 6 months. That’s not “quit your job” money, but it’s “pay off your credit card” or “build an emergency fund” money. And that matters.

The Tools and Habits That Kept Me Going Past Month Three

The first three months of any side hustle are the hardest. You’re putting in time, seeing almost no return, and your brain is screaming at you to quit. I almost quit three times. Here’s what kept me in the game.

Tracking every dollar. I opened a separate checking account just for side hustle income and expenses. No mixing with my day job money. Seeing the balance grow (even by $45 at a time) was addictive in a good way. I also tracked hours using Toggl so I knew my real hourly rate.

Setting a “quit number.” I told myself I wouldn’t give up until I hit $500 in a single month. That gave me a specific target instead of a vague “make more money.” I hit $500 in month four. Then I set the next target at $1,000. I’m still working toward that second number.

Finding one accountability partner. I joined a small Discord server for freelancers. One guy named Marcus and I started checking in daily — “what’d you do today, how much did you earn, what’s tomorrow’s goal.” Having someone who’d notice if I disappeared kept me showing up on days I wanted to binge Netflix instead.

What I’d Do Differently If I Started Today

Looking back at everything I messed up, here’s my honest advice:

Start with a service, not a product. Services pay you immediately. Products pay you eventually. When you have no money, take the immediate cash and build from there. My biggest mistake was chasing “passive income” before I had any active income.

Pick one thing and go deep for 90 days. I bounced between six different side hustles in my first year. Each time I started something new, I was back at zero. The people I see succeeding in 2026 are the ones who picked one lane (freelance writing, dog walking, whatever) and stuck with it for 90 days minimum before deciding it didn’t work.

Ignore anyone selling a course before they show results. If a “guru” has a $500 course but can’t show you their actual bank statements or client work, run. Real side hustlers show receipts. I learned this the hard way three times.

Invest your first $200 in tools, not “education.” A $10 domain, a $15 Canva subscription, and a $5 Notion template will do more for your side hustle than a $2,000 coaching program. I spent $3,400 on “education” that taught me nothing and $50 on tools that actually generated income.

If you’re starting a side hustle in 2026, the move is simple: pick one skill people will pay for, offer it cheap at first to build proof, then raise your rates every 60 days. Don’t buy courses. Don’t chase trends. Just do the work and keep track of what’s working. It took me a year and a lot of expensive mistakes to figure that out, but you don’t have to make the same ones.

When people say “side hustle,” I imagine someone grinding on Fiverr at 2 AM, posting TikTok videos about dropshipping, or walking dogs in the rain. I’ve tried that. It’s exhausting.

So I tried the opposite. I built income streams that required zero active work after the setup. No client calls. No invoices. No hustling. Here’s what actually worked.

What I Did Instead of Grinding

After my earlier side hustle experiment, I realized I was trading time for money. Every dollar came from active work. That’s not a side hustle — that’s a second job.

I wanted passive income. Not “get rich on a beach” passive, but “earn $400 monthly without thinking about it” passive.

Income #1: Affiliate Links From Stuff I Already Owned

I wrote three honest reviews of products I actually use and posted them on a simple blog. No SEO strategy, no content calendar. Just: “I use this, here’s why, here’s the link.”

Month one: $64. Month three: $210. Current monthly average: $180. The posts took about 4 hours total to write. They’ve earned over $800 collectively.

I use Amazon Associates and a few niche affiliate programs. The key: only promote things I genuinely recommend. The income is a byproduct, not the goal.

Income #2: Digital Products From One Weekend of Work

I created a simple budget spreadsheet in Google Sheets — the same one I use for my own finances — and sell it on Gumroad for $9. It took one Saturday to build and format.

I’ve sold 48 copies in 7 months. That’s $432 minus Gumroad’s fee. I’ve done zero marketing. People find it through my blog posts about budgeting.

The math: if I can get this to 10 sales per month consistently, that’s an extra $800/year for work I did once.

Income #3: Selling Old Stuff Properly

Instead of garage sales or donating, I checked eBay sold prices for my old electronics, books, and kitchen gear. The difference was eye-opening.

A stand mixer I was going to donate? Sold for $85. Old textbooks? $42 total. A camera I hadn’t used in three years? $220.

Total from one weekend of photographing and listing: $430. Time invested: about 6 hours.

Why This Works Better Than Grinding

Each of these took setup time but generates income without ongoing effort. I don’t answer client emails. I don’t negotiate rates. I don’t have to post content on a schedule.

My total passive-ish income last month: $450. Not enough to quit anything, but enough to cover my phone bill, streaming subscriptions, and a dinner out without touching my main budget.

TL;DR

Affiliate links from honest reviews of things you own: low effort, compounding returns

Digital products (templates, guides, spreadsheets): one-time work, sells forever

Sell old stuff properly — check eBay sold prices, don’t just donate

Passive income doesn’t mean zero work; it means work once, earn many times

The goal isn’t to get rich on the side. The goal is to make your main income go further.

I had $8,500 spread across three credit cards. Not the worst debt story you’ll hear, but it was eating $200/month in interest and making me feel like I was running on a treadmill.

I’d already paid off $12,000 in debt before (that story is on the site), but I slipped again during the holidays. Wedding gifts, flights, a few nights out that turned into $600 on my card. It adds up fast when you’re not tracking.

This time, I did the debt snowball method. Here’s how it actually went.

What the Debt Snowball Is (And Why It Works)

You list all your debts from smallest to largest. You pay the minimum on everything except the smallest debt, which you attack with every extra dollar. When the smallest is gone, you roll that payment to the next smallest.

Critics say the avalanche method (highest interest rate first) saves more money. They’re right. But the debt snowball isn’t about math. It’s about momentum. And momentum is what I needed.

My Debt List When I Started

Card A: $1,200 at 22% APR (minimum: $35/month)

Card B: $3,800 at 19% APR (minimum: $85/month)

Card C: $3,500 at 24% APR (minimum: $80/month)

Total minimum payments: $200/month. Interest per month: roughly $170.

Month 1-3: Killing Card A

I threw $400 extra at Card A every month by cutting subscriptions and eating out less. That’s $400 + $35 minimum = $435/month.

Card A was gone in 3 months. I felt like I’d won a small war. The $35 minimum was now freed up to attack Card B.

Month 4-7: Attacking Card C (The Highest Rate)

I went after Card C instead of Card B because Card C had the highest interest rate (24%). I broke the pure snowball rules and attacked the most expensive debt first after the smallest was gone. Hybrid strategy.

I was now throwing $400 + $35 (freed up) = $435 at Card C each month. Plus the $80 minimum. Total: $515/month.

Card C went from $3,500 to $1,200 over four months.

Month 8-10: Finishing Card C and Starting Card B

Card C was paid off in month 8. Now I had $435 + $80 = $515 freed up, plus the original $85 minimum on Card B. Total attacking Card B: $600/month.

Card B balance: $3,800. Gone in about 3 months.

By month 10, all three cards were paid off.

The Real Cost

Total interest paid during the snowball: roughly $640. Not great, but better than the $1,700 I would’ve paid at minimum payments over 3 years.

Total saved from the original $8,500 in interest just from paying aggressively: about $1,000.

TL;DR

Debt snowball = smallest balance first for psychological wins

I hybridized it: snowball to build momentum, then avalanche for the expensive stuff

$435/month extra + freed up minimums = $8,500 gone in 10 months

Paid $640 in interest instead of $1,700+ — a $1,000 win

The best debt strategy is the one you’ll actually stick with.

I didn’t know what a Roth IRA was until I was 29. Let me be straight with you: I spent my 20s thinking retirement accounts were something other people set up. The ones with stable jobs, 401(k) matching, and retirement calculators on their nightstands.

I was self-employed, making around $48K a year, and every dollar felt accounted for. Rent, groceries, insurance, the occasional pizza delivery that turned into a $45 regret. Retirement felt like a luxury I couldn’t afford.

Then my friend Sarah — who makes less than I do — told me she’d put $3,000 into a Roth IRA that year. I asked how. She said she automated it. That word changed everything.

What a Roth IRA Actually Is (No Finance Degree Required)

A Roth IRA is a retirement account where you put in after-tax money, it grows tax-free, and you don’t pay taxes when you withdraw it in retirement. The key number: you can contribute up to $7,000 in 2025 ($8,000 if you’re 50+). That’s about $134 a week.

What I didn’t realize is that you can withdraw your contributions (not the earnings) at any time without penalty. That’s a safety net I didn’t know I had. It made the decision to start way less scary.

I use Vanguard because their fees are low and the interface isn’t trying to sell me stuff. Fidelity and Schwab are equally solid. Pick one and move on.

How I Opened Mine in 30 Minutes

I picked Vanguard. The whole process took less time than I spend deciding what to order for dinner. They ask for your Social Security number, bank account info, and beneficiary. That’s it.

I put in $500 to start because I had it. The minimum for most target-date funds is $1,000, so I bought an ETF instead (VTI, total stock market). Fees: 0.03% per year. That’s $3 for every $10,000 invested.

The Automated Strategy That Actually Works

Here’s the part that made it stick: I set up auto-transfers of $100 every Monday morning. Not monthly. Weekly. The psychology difference is real — $100 disappearing weekly feels like a phone bill, not a sacrifice.

I also round up purchases through an app called Acorns for the first three months. That gave me an extra $40–60/month without thinking about it. After three months, I stopped and put that amount into the IRA instead.

What Happened After 18 Months

Total contributions: $9,000. Total value: $11,200. The market was good, but even if it wasn’t, I would’ve kept contributing because time in the market beats timing the market. Yeah, that’s a cliché because it’s true.

The real win wasn’t the $2,200 in gains. It was that I stopped treating investing like a future-me problem. I started feeling like someone who had their act together.

The Mistake I Made (So You Don’t Have To)

I tried to pick individual stocks for three months. I bought Tesla at $260, sold at $245. Then bought Apple at $178, sold at $182. After fees and stress, I made maybe $60. Total waste of energy.

Index funds or target-date funds are the answer. Set it, forget it, and check once a year. Your future self will thank you for being boring.

TL;DR

Roth IRA = after-tax money, tax-free growth, cap of $7,000/year in 2025

Open one at Vanguard/Fidelity/Schwab — takes 30 minutes

Set up weekly auto-transfers, buy index funds, don’t touch individual stocks

You can withdraw contributions anytime without penalty (not that you should)

I’m not a financial advisor. Just someone who wishes they started earlier.

What you will learn: What a no-spend month actually involves, the surprising challenges I didn’t expect, and whether the savings are worth the effort.

Money Fast: The Experiment

I had heard about “no-spend months” where people only buy essential items for 30 days. No eating out, no shopping, no entertainment. I was skeptical but curious. Could I survive a month without spending money on anything unnecessary?

The rules I set: I could pay rent, utilities, insurance, and buy groceries. Everything else was banned. No coffee shops, no restaurants, no Amazon, no bars, no movies. If it wasn’t a bill or food I cooked myself, I couldn’t buy it.

Week 1: The Easy Part

The first week was surprisingly easy. I had groceries in the fridge, no urgent needs, and the novelty of the challenge kept me motivated. I cooked every meal, drank free coffee at work, and entertained myself with books and walks. By day 7, I had saved roughly $200 compared to a normal week.

Week 2: The Temptation Hits

Week two was harder. My friends invited me to dinner. I had to say no. I ran out of my favorite snack and couldn’t replace it. I wanted to buy a book I was excited about. The restrictions started to feel real.

I realized how much of my social life revolved around spending money. Saying “no” to dinner meant saying “no” to seeing friends. I started suggesting free alternatives: hikes, potlucks, game nights. Some friends were into it. Others thought I was being dramatic.

The Result

I completed the full month. Total non-essential spending: $0. I saved $740 compared to my average month. The biggest surprise was how much I didn’t miss. The coffee shop runs, the impulse Amazon purchases, the spontaneous dinners out. Most of them were habits, not genuine needs.

Would I do it again? Yes, but not every month. A no-spend month once or twice a year resets your spending habits and shows you how much you waste on autopilot. The lessons I learned about my own spending patterns lasted long after the month ended.

What you will learn: Why most tenants never negotiate rent (and why you should), the exact email script I used, and what to say when they say no.

Rent Is Your Biggest Expense, So Fight It

I had been living in the same apartment for three years. My rent had increased by $200 total over that period. When my lease renewal came with another $75 increase, I decided to try something I had never done before: negotiate.

I was terrified. I imagined my landlord laughing at me, or worse, deciding not to renew my lease. But I did my research and discovered something encouraging: in most markets, landlords prefer a reliable tenant at slightly below market rate over the uncertainty of finding a new one.

The Research Phase

Before reaching out, I spent two hours on Zillow and Apartments.com checking what comparable units were renting for in my building and neighborhood. I found three units similar to mine renting for $200-$300 less per month. I also noted that my building had a 92% occupancy rate, which meant there was some vacancy, giving me leverage.

The Email That Worked

I sent a polite email to my property manager. The key elements: I expressed my desire to stay. I mentioned my three-year history of on-time payments. I cited specific comparable listings. And I asked for a specific number.

Here is roughly what I wrote: “Hi [Manager], I have loved living here for the past three years and would like to renew. However, the proposed increase brings my rent above similar units in the area. Based on my research, I would like to request keeping my rent at $1,275 (the current rate) rather than increasing to $1,350. I have been a reliable tenant and would love to stay for another year. Thank you for considering this.”

The Result

My property manager replied within 24 hours. She offered a compromise: keep the rent at $1,275 but extend the lease to 15 months. I accepted immediately. I saved $75/month, which is $900 over the lease term.

The next year, I used the same approach and negotiated a $50 reduction by pointing out that a similar unit in the building had been vacant for six weeks. Total savings over two years: $2,100. For two hours of research and a 10-minute email.

What you will learn: Why traditional emergency fund advice is wrong for most people, a realistic savings timeline, and how to make the process painless.

The $1,000 Starter Fund Changed Everything

Every financial expert says you need 3-6 months of expenses in an emergency fund. That is great advice for someone who already has their finances together. For someone living paycheck to paycheck, that advice is not just unhelpful. It is paralyzing.

When I had $237 in my account, the idea of saving $15,000 felt impossible. So I didn’t try. I didn’t save anything. Why bother when the goal was so far away?

Start With $1,000

I read somewhere that $1,000 covers most common emergencies. Car repair. Minor medical bill. Emergency flight. Not a job loss, but the small emergencies that keep you stuck in the paycheck-to-paycheck cycle.

I set a goal of $1,000. I saved aggressively for two months. I sold things, cut eating out, and worked extra hours. When I hit $1,000, I felt richer than I ever had with a $5,000 credit limit.

Then $3,000

Once I had $1,000, the next goal felt achievable. Three thousand would cover one month of expenses. I automated $200 per paycheck and stopped thinking about it. Seven months later, I hit $3,000.

The Anti-Budget System

I didn’t use a strict budget to save my emergency fund. Instead, I used what I call the “anti-budget.” I automated my savings and paid my bills. Everything left in my checking account was guilt-free spending money. I didn’t track categories or worry about overspending on coffee. The automation did the work for me.

It took me 14 months to save $5,000 (about 3 months of expenses). That is slower than the experts recommend, but it happened because it was sustainable. An emergency fund that takes 14 months to build is infinitely better than a perfect plan you abandon after two weeks.